Why Commodity Regulators Track Trade Reports

Why Commodity Regulators Track Trade Reports

Commodity regulators track trade reports for one reason: to see market risk and bad behavior before it turns into a bigger problem.

If I had to sum up the article in plain English, it’s this: regulators use trade and position data to check who traded, what they traded, how much, at what price, when it happened, and where it happened. That helps them watch for large concentrated positions, possible manipulation, and missing or late reports. If the data is wrong, the regulator’s view is wrong too.

Here’s the short version:

- Large trader reports show when one firm or client may hold too much of a market

- Swap and position reports help regulators track OTC and cleared exposure

- Timestamps, venue data, and lifecycle events help rebuild what happened in a trade

- IDs like account numbers and LEIs show who is behind the position

- Price and valuation fields help analysts test whether a trade fits market conditions

- Daily reconciliations and audit logs help firms explain every report to the CFTC or NFA

- Deadlines matter: large trader reports are due by 9:00 a.m. the next business day

- Bad controls can lead to fines; the article cites a $1.5 million CFTC penalty tied to position-limit and supervision failures

What matters most to me as a reader is simple: this is not just a filing task. It’s a daily data-control job tied to surveillance, reconciliation, recordkeeping, and price checks across markets like WTI crude, Brent, natural gas, and gold.

The main takeaway: clean, on-time trade reporting helps regulators spot concentration, abusive patterns, and data breaks fast - and helps firms defend their records when questions come in.

The Complete Guide to Commodity Trade Compliance

What regulators look for in trade reports

Regulators use trade reports to test three things: market power, abusive patterns, and data quality. After firms file reports, regulators review them for size, behavior, and whether the data holds up.

Large positions, concentration, and position-limit exposure

The CFTC's surveillance staff watches the daily activity of large traders, key price relationships, and supply-and-demand factors to spot manipulation and protect market integrity. One of the first things they check is concentration, including how much open interest the largest four or eight traders hold in a contract month.

If a trader hits a reportable level in one contract month, the firm has to report that trader's entire position across all months for that commodity, not just the month that triggered the filing. That gives regulators a full view of long and short exposure.

This matters a lot in physical-delivery contracts like WTI crude or Henry Hub natural gas. A dominant position near expiry can point to cornering or squeeze risk, especially if the trader also controls related physical supply, such as storage or pipeline capacity. The CFTC's large-trader data flows into its Integrated Surveillance System (ISS), where positions are tied to ownership and control information for special accounts. From there, regulators can look past raw size and study whether the activity makes sense.

Patterns linked to manipulation or abusive trading

Size alone doesn't tell the whole story. Regulators also review behavioral patterns in order and execution records.

Spoofing tends to show up as large orders that are placed and then canceled fast, often right before aggressive trades on the other side. Wash trades tend to appear as offsetting buys and sells between related accounts at similar prices and sizes, often near reporting deadlines or settlement windows. Regulators also watch for settlement-period volume spikes or price moves that help a trader's larger position.

Execution timestamps matter here. They let regulators line up trading activity against price-sensitive events, such as EIA inventory releases.

Completeness, accuracy, and timeliness of submissions

Regulators also test whether reports are complete, accurate, and on time. Completeness means all reportable trades, venues, lifecycle events, and accounts are included. Accuracy is checked against exchange feeds, clearing records, and market prices.

Timeliness matters because regulators need current data, not stale files. Large-trader reports are due by 9:00 a.m. on the business day after the report date. Miss that deadline, and it's a compliance breach. Missing trades, bad mappings, or late submissions can trigger enforcement. Recent CFTC actions against major banks and trading venues show that risk.

Those checks all depend on the details inside each report, especially the contract, trader, and execution data.

Which trade report fields matter most

Once you know what regulators look at, the next step is simpler: know which fields let them rebuild the trade from the ground up. In practice, regulators zero in on the fields that identify the trade, the parties, and the exposure. If those fields are off, the whole picture can drift. That’s why analysts should treat them as the first validation layer in every daily and end-of-day file.

Instrument, contract month, side, and quantity

The instrument identifier ties the trade to the right underlying market and contract type. Get that code wrong, and the position lands in the wrong reporting bucket.

Contract month sets the delivery window and the position-limit period. If a trade is booked to August instead of September, it can skew expiry risk and position-limit exposure. The side field shows whether the position is long or short, and quantity fills in the rest. Quantity should match both the contract count and the commodity’s physical unit. Analysts should also check that notional amounts use the right price and currency.

Surveillance looks at gross exposure, not netting, when spotting concentration risk.

Trader, account, client, and counterparty identifiers

Trader IDs, account numbers, client IDs, and counterparty LEIs show who holds the position. Account numbers need to clearly separate proprietary positions from client accounts, and that mapping has to stay consistent across front-office, risk, and back-office systems. If an intermediary sits between the reporting firm and the end client, many reports still need to trace the position back to the underlying client.

Counterparty identifiers standardized through Legal Entity Identifiers (LEIs) show regulators whether the other side is a clearing house, another dealer, a corporate hedger, or a fund. Entity type matters as well. A commercial hedger and a financial firm do not carry the same regulatory meaning, and if one is tagged as the other, the aggregate view regulators use to separate hedging from speculative activity gets distorted. Analysts should check that reporting-system classifications still line up with current KYC data and business activity.

Execution time, venue, lifecycle event, and valuation

Execution timestamps should be consistent and in U.S. Eastern Time - for example, 07/10/2026 14:35:27. That helps regulators line up reported trades with order books and price feeds when they check whether activity matches market conditions.

Venue flags show whether a trade happened on an exchange, a swap execution facility (SEF), or bilaterally OTC. Each one comes with different reporting duties, so a bad venue tag can put the trade under the wrong rule set. Lifecycle event fields - new, amended, partial termination, compression, novation - show how a position changes from open to close. Without those fields, a position cut down through partial terminations might still look open in a snapshot view.

Valuation fields, including trade price, mark-to-market value, and notional amount, should reconcile with internal risk systems and daily market prices. Reported valuation currency should be in USD and formatted the same way each time, for example $1,250,000.00. When timestamps and valuations line up, analysts can test whether reported activity fits the market. Those same fields also help with price checks and transparency reviews.

sbb-itb-a92d0a3

How trade reporting supports price transparency

Trade reports don't set prices. But they do shape the information around those prices.

When firms send standardized reports to central repositories, regulators get one joined-up view of transaction volume, open positions, and how prices shift as trades happen across futures, options, and physical contracts. That view lets them test whether price moves line up with reported activity. Of course, that only works when reports and price data are standardized enough to match cleanly.

Trade repositories and aggregate position reporting

Trade repositories bring standardized data from many venues into one place and give regulators a single market view. They can show volume, concentration, and exposure by trader category. The CFTC's weekly Commitments of Traders reports, for example, group open interest by trader category without naming individuals.

CPMI/BIS and IOSCO also back periodic publication of aggregate open-interest and volume data to improve transparency. For that comparison to hold up, the underlying data needs clean timestamps, correct contract codes, and consistent reporting fields.

Using price data to check whether reported activity fits market conditions

Aggregate position data shows who holds what. Price data shows whether that activity makes sense in the market.

Compliance teams can match each trade's instrument, side, quantity, and timestamp to the benchmark price at execution. That makes it possible to measure slippage and flag trades done at unusual premiums or discounts.

For energy markets, OilpriceAPI provides real-time and historical Brent, WTI, Natural Gas, and Gold prices for timestamp checks and benchmark comparisons.

If the same price gaps show up again and again without a clear commercial reason, that should be documented and escalated. Pairing trade data with price feeds and repository totals helps compliance teams spot mismatches fast. These checks work best when firms standardize formats and reconcile exceptions daily.

Practical compliance steps for analysts

Commodity Trade Reporting: Key Fields, Controls & Compliance Steps

Once regulators can line up reported activity with market prices, the next test is simple: can the firm stand behind every single record?

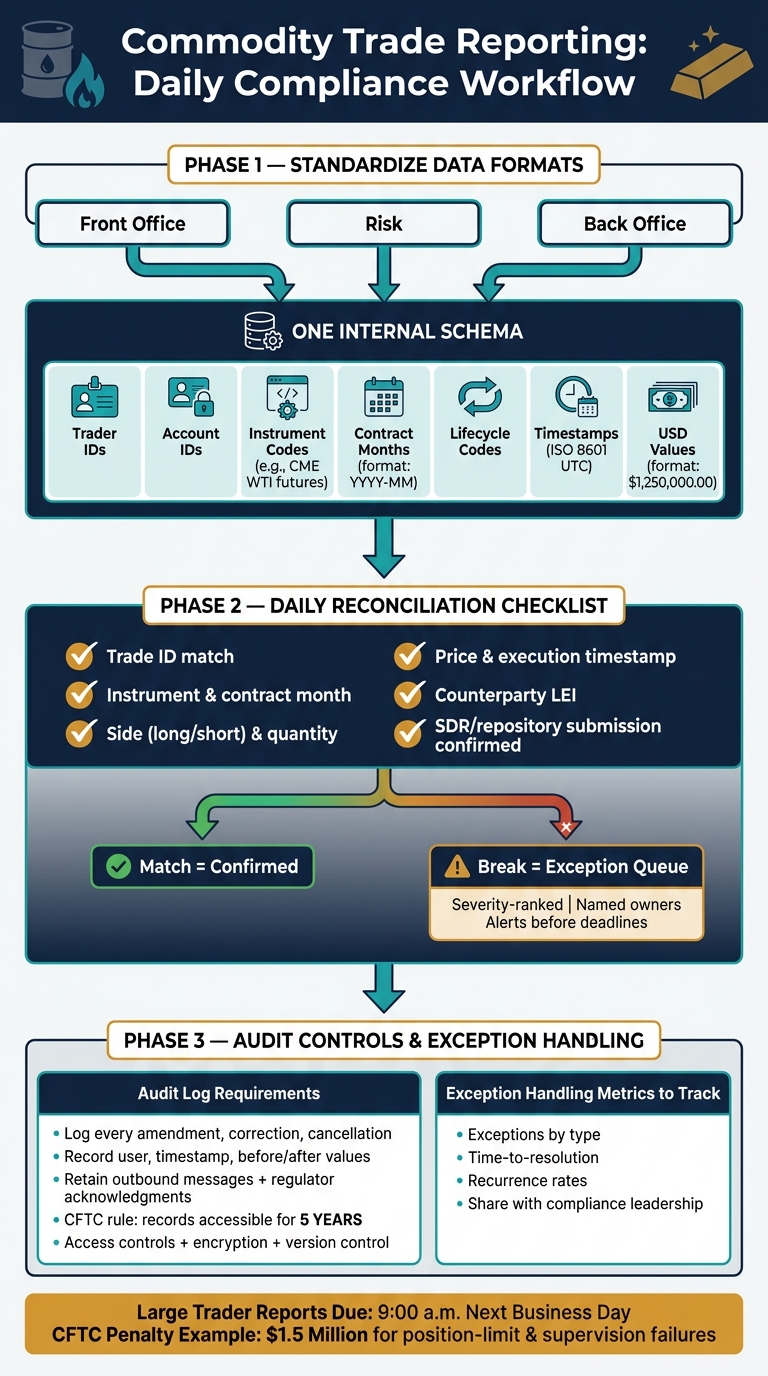

Standardize data formats and reconcile across systems

Use one internal schema across front office, risk, and back office. Define trader IDs, account IDs, client IDs, instrument codes, contract months, lifecycle codes, timestamps, and USD values once, then use those same definitions everywhere.

Keep timestamps in ISO 8601 UTC and convert to local time only when someone needs to view them. Contract months should use YYYY-MM, and instrument codes should match exchange conventions - for example, CME contract codes for WTI futures - so submissions line up with what swap data repositories and regulators expect.

Reconcile data every day. Compare the booking system with what was sent to the SDR or trade repository. Check trade ID, instrument, side, quantity, price, execution time, and counterparty. If something breaks, send it into a severity-ranked exception queue with clear resolution steps written down.

After matching and reconciliation, audit logs keep the reporting trail intact.

Build controls for auditability and exception handling

Log every amendment, correction, or cancellation with the user, timestamp, and before-and-after values. Keep outbound messages to regulators, plus any acknowledgments, rejections, and resubmissions, so you can rebuild the full reporting history for any trade on demand.

CFTC recordkeeping rules say electronic records must stay readily accessible for five years. Access controls, encryption, and version control all belong in the recordkeeping program regulators expect to review.

When exceptions show up, speed matters more than sheer volume.

Put exception handling in one place. Route late reports, rejected submissions, missing fields, price outliers, and timestamp anomalies into a single queue with severity levels and named owners. Set alerts to go off well before regulatory deadlines. Track metrics like exceptions by type, time-to-resolution, and recurrence rates, then share them with compliance leadership. Those numbers show active control, not passive cleanup.

Conclusion: accurate reports support fair and transparent commodity markets

For U.S. commodity analysts, the day-to-day focus comes down to three things: data quality, timeliness, and price-linked validation. In practice, that means standard fields, reconciled systems, automated pipelines tied to regulatory deadlines, and independent price data - such as real-time and historical Brent, WTI, Natural Gas, and Gold feeds from OilpriceAPI - to check whether reported trades fit observable market conditions.

Clean reporting makes surveillance more believable and helps keep commodity markets fair and transparent.

FAQs

How do regulators tell hedging from speculation?

Regulators use trade reports to judge a position’s intent and the risk behind it. Hedging must connect to a real commercial need, such as managing exposure to swings in energy prices.

To check that, they look at standard price benchmarks and audit trails. The goal is simple: confirm that trades match physical asset ownership or actual production needs.

OilpriceAPI can help support that review by providing historical and real-time commodity data for:

- compliance reporting

- mark-to-market valuations

- position monitoring

What happens if a trade report is late or wrong?

A late or inaccurate trade report can weaken market oversight and create compliance problems. That’s where validation rules come in. They help catch odd data points or source errors before submission, often flagging them or holding publication until someone checks the details.

Direct API integration cuts down on manual work, which means fewer chances for human error. On top of that, an audit trail with historical data gives teams a clear record to review, making it easier to spot and fix reporting gaps fast.

Why do timestamps and prices matter so much?

Timestamps and prices sit at the heart of regulatory oversight and market transparency. Precise timestamps let regulators rebuild the exact sequence of events, support market integrity, and create clear audit trails.

Paired with accurate price data, they also help analysts check fair market value and carry out mark-to-market valuations. Standardized data, along with consistent source timestamps and freshness metadata, supports reliable compliance reporting.